TARGET2 Imbalances: Causes And Consequences

TARGET2 is the European System of Central Bank’s (ESCB) balance of payments mechanism. The acronym stands for Trans-European Automated Real-time Gross settlement Express Transfer system. The purpose of TARGET2 is to provide a mechanism for the real-time gross settlement of cross-border interbank and customer payments. The system allows for intra-day finality, which

insures that transactions will not be unwound if one of the parties fails to settle.

TARGET2 has recently been the subject of much attention given large imbalances that have appeared between net creditor NCBs (National Central Banks), such as the Bundesbank, and net debtor NCBs, such as the Bank of Ireland. Some have claimed that these imbalances are a “stealth-bailout” of the periphery by the core. Others claim that these imbalances are leading to restricted liquidity and possibly the need to sell NCB assets in the creditor nations. I shall humbly attempt to address these issues and explain how TARGET2 works. At the end, I will raise what I feel are concerns stemming from the existence of these imbalances.

How does TARGET2 work?

The system itself is rather complicated, and an understanding of it demands knowledge of what represents a bank asset versus a bank liability. For a non-bank commercial corporation, an asset is obviously something it owns, like plant, equipment, inventory, etc. The corporation’s liabilities are things which it owes, like loans, payroll, pension obligations, etc. For a bank, the situation is reversed. A bank’s liabilities are things it owes to others, such as demand deposits, while its assets are those things which are owed to it, such as loans.

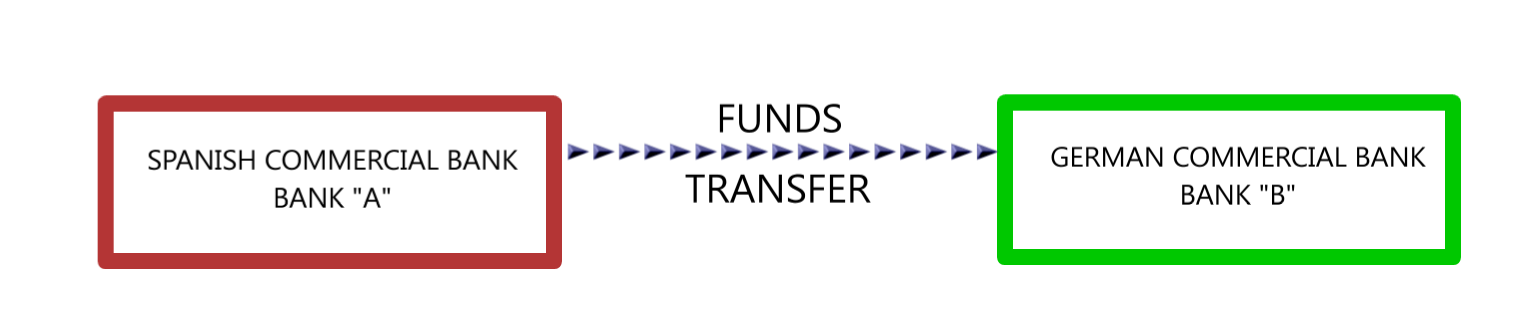

With that background, let’s look at an example of a funds transfer from a Spanish commercial bank (Bank “A”) to a German commercial bank (Bank “B”). This transfer could either be a payment from one of the Bank A’s account holders to a German corporation with an account at Bank B, or it could be the transfer of one of Bank A’s demand deposit accounts to Bank B.

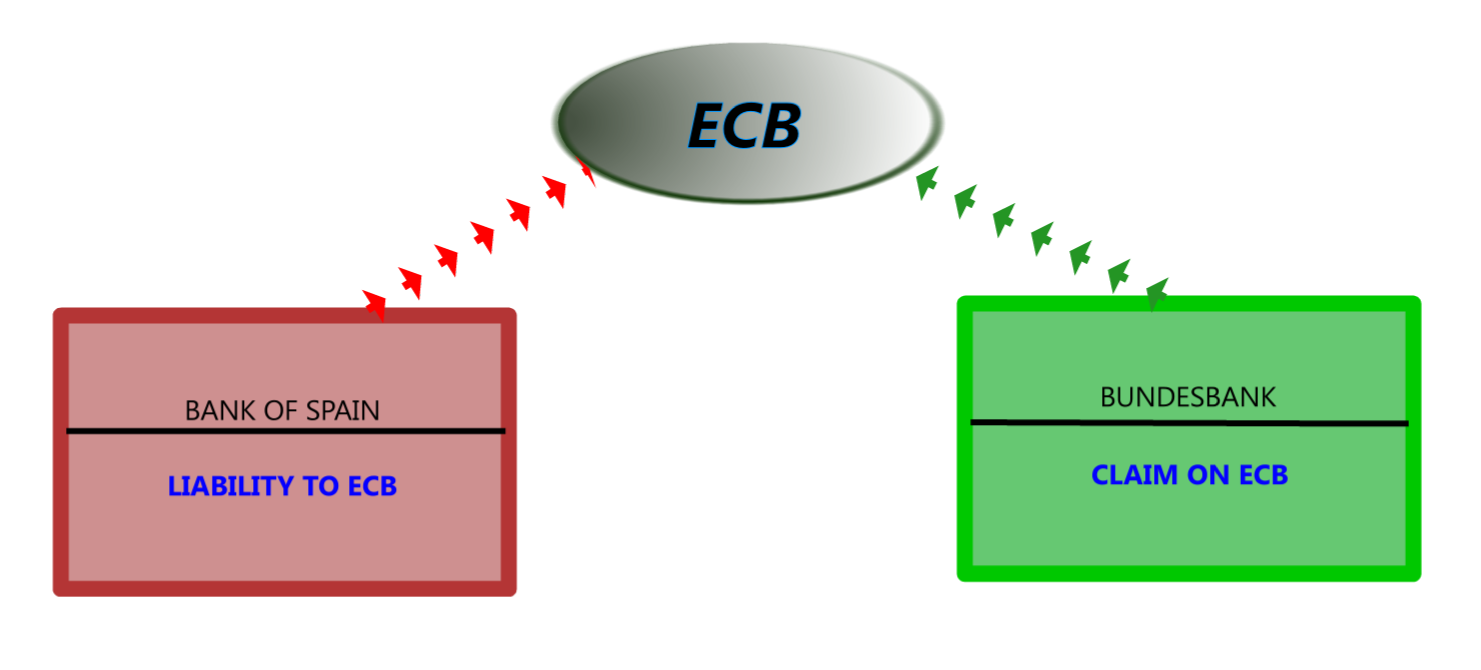

TARGET2 performs this transfer by debiting the Spanish bank’s account at the Bank of Spain, and crediting the German bank’s account at the Bundesbank. Note – the transfer occurs at the NCB level.

| THE CRUX OF THE MATTER |

The Bundesbank’s liability to Bank B is matched on the asset side of the balance sheet in the form of a claim on the Bank of Spain, just as the Bank of Spain’s credit from Bank A is matched by a liability to the Bundesbank.

At the end of the transaction, the two NCB’s positions are as shown below.

Why So Much Imbalance?

Imbalances in a gross payment system like TARGET2 are nothing unusual. In the past, NCBs usually displayed non-zero TARGET2 balances vis-à-vis the ECB, but the balance tended to be neutral on average. However, in the last few years some countries have seen their TARGET2 liabilities increase (and conversely others have seen their TARGET2 claims increase) up to six-fold or more. This chart from a MUST-READ note by Credit Suisse (CS) illustrates the problem as of Q3:2011.

To understand why this has occurred, let me take you back to that transaction I highlighted above (labeled as “The Crux of the Matter”), in which the Bank of Spain debits the account of the Spanish commercial bank – Bank A. In years past, that Spanish commercial bank, as well as most other banks in peripheral Europe, had ready access to private funding, often on an unsecured basis. That funding came from US Money Markets, direct investments, and interbank loans – often from commercial banks in the surplus countries of Europe, like Germany. Access to this private, largely unsecured funding is what allowed peripheral banks to pay off their liabilities to their respective NCBs.

However, starting in mid-2010 with the first stirrings of the Greek crisis, investors and depositors began to differentiate between the perceived risks of banks in the periphery versus the core, and this trend has done nothing but accelerate since. According to Fitch, US money market funds (MMF) reduced their exposure to European banks by over 45% in this year alone, and the remaining financing has migrated to much shorter duration instruments.

Additionally, the nature of the MMF funding has changed. MMFs have reduced their unsecured lending, partially replacing it with secured repo financing against collateral. (FT)

Furthermore, German banks have drastically cut their lending to the periphery, as is shown in the graph below, from the Bundesbank.

In summary, we now have a situation in which the interbank market is dysfunctional, cross border loans have decreased and deposits are flowing out of the crisis countries. As a result, these net capital outflows settled through the national central banks result in the respective NCBs accumulating TARGET2 liabilities on their balance sheets, while the countries receiving the flows (e.g. Germany) accumulate TARGET2 claims. Peripheral banks can no longer fund themselves through the private markets, and it is the peripheral NCBs that now provide the funding in the form of secured loans against collateral.

To explain further, I find it hard to do better than quoting directly from the Credit Suisse paper.

“Due to the flight of liquidity from banks in the periphery, the ECB has stepped in and provided the liquidity, in the form of unlimited provision of funding to the banks against collateral – i.e., through MROs and LTROs.

For that reason NCBs’ balance sheets that show increased TARGET2 liabilities vis-à-vis the ECB, generally also display increased liquidity provisions through lending operations on the asset side. The ECB stepped in to play the role of liquidity provider when there was limited flow of private funds to crisis countries and increased TARGET2 liabilities largely reflect that.

The extent to which TARGET2 reflect these imbalances in liquidity needs across the euro area is demonstrated by Exhibit 5. It shows the refinancing operations (MROs and LTROs) on the balance sheet of the Bundesbank and the NCBs of the five peripheral economies. TARGET2 imbalances became increasingly noticeable not during the 2008-2009 crisis, when both Germany and the periphery required liquidity, but after 2010, when German liquidity needs sharply dropped away and the needs of the periphery continued to increase. This is shown clearly in Exhibit 6, which charts the difference between the value of the refinancing operations in the periphery and Germany against Bundesbank TARGET2 claims.

So the underlying factor driving the expansion of TARGET2 liabilities in the periphery is that capital outflows have intensified since the crisis, while the willingness of the private sector to finance these flows has decreased. This can be shown in Exhibits 7 and 8, which chart the behavior of the current account and TARGET2 imbalances in the periphery and Germany. Exhibit 7 shows that between 2007 and 2011 the periphery’s current account deficit has more or less been maintained, but the source financing this has switched from the private sector to ECB financing.”

Hopefully, you now understand how these imbalances have arisen. I would also hope that it is clear that these imbalances are NOT the result of a deliberate stealth bailout of the periphery by the surplus NCBs. Instead the imbalances are a reflection of the funding difficulties in the periphery and are more driven by the actively derived negative balances of the peripheral NCBs than by the passively derived positive balance of the Bundesbank. (An important and related aspect of TARGET2 is that, while an NCB can place a credit limit on the TARGET2 balance of a commercial bank or other MFI, it cannot place such a limit on one of its fellow NCBs.)

Is There A Limit to TARGET2?

The short answer here is no. However, from a practical standpoint, the amount of eligible collateral that peripheral commercial banks can pledge to their NCBs is limiting. This is one of the main reasons the ECB recently relaxed collateral rules, expanded collateral eligibility, reduced reserve requirements, and expanded repo operations. Should losses be realized in the TARGET2 system as a consequence of a country default or exit, we could see positive balance NCBs (like the Bundesbank) demand a re-tightening of collateral eligibility rules, as well as the imposition of TARGET2 credit limits on some commercial financial institutions.

What are the Risks?

Let’s start with the case of the Bundesbank, as they hold the largest TARGET2 credit position, by far. As of November 30, 2011, the balance was 495,164.155 Euros! The graph below charts its progress, and has undoubtedly shown explosive growth since the late December LTRO by the ECB.

-

buy five 100 € lower yielding short term issues that have a 5% haircut, giving you 475 € of collateral, or

-

buy ten 50 € higher yielding longer term issues that have a 10% haircut, giving you 450 € of collateral?

Source:

Anyone can join.

Anyone can contribute.

Anyone can become informed about their world.

"United We Stand" Click Here To Create Your Personal Citizen Journalist Account Today, Be Sure To Invite Your Friends.

Before It’s News® is a community of individuals who report on what’s going on around them, from all around the world. Anyone can join. Anyone can contribute. Anyone can become informed about their world. "United We Stand" Click Here To Create Your Personal Citizen Journalist Account Today, Be Sure To Invite Your Friends.

LION'S MANE PRODUCT

Try Our Lion’s Mane WHOLE MIND Nootropic Blend 60 Capsules

Mushrooms are having a moment. One fabulous fungus in particular, lion’s mane, may help improve memory, depression and anxiety symptoms. They are also an excellent source of nutrients that show promise as a therapy for dementia, and other neurodegenerative diseases. If you’re living with anxiety or depression, you may be curious about all the therapy options out there — including the natural ones.Our Lion’s Mane WHOLE MIND Nootropic Blend has been formulated to utilize the potency of Lion’s mane but also include the benefits of four other Highly Beneficial Mushrooms. Synergistically, they work together to Build your health through improving cognitive function and immunity regardless of your age. Our Nootropic not only improves your Cognitive Function and Activates your Immune System, but it benefits growth of Essential Gut Flora, further enhancing your Vitality.

Our Formula includes: Lion’s Mane Mushrooms which Increase Brain Power through nerve growth, lessen anxiety, reduce depression, and improve concentration. Its an excellent adaptogen, promotes sleep and improves immunity. Shiitake Mushrooms which Fight cancer cells and infectious disease, boost the immune system, promotes brain function, and serves as a source of B vitamins. Maitake Mushrooms which regulate blood sugar levels of diabetics, reduce hypertension and boosts the immune system. Reishi Mushrooms which Fight inflammation, liver disease, fatigue, tumor growth and cancer. They Improve skin disorders and soothes digestive problems, stomach ulcers and leaky gut syndrome. Chaga Mushrooms which have anti-aging effects, boost immune function, improve stamina and athletic performance, even act as a natural aphrodisiac, fighting diabetes and improving liver function. Try Our Lion’s Mane WHOLE MIND Nootropic Blend 60 Capsules Today. Be 100% Satisfied or Receive a Full Money Back Guarantee. Order Yours Today by Following This Link.

| Visits: | 1,826,454,105 |

| Stories: | 8,680,019 |

Whistler Blowers, Insiders

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}