Does J Sainsbury deserve to be a Super Stock?

The UK’s second-largest supermarket trades at a discount to book value and offers a 5% dividend.

Shares in J Sainsbury (LON:SBRY) have fallen by around 15% since the start of the year, but trading seems solid and Stockopedia’s algorithms rate this retailer as a Super Stock.

With full-year results due in April, I think it could be a good time to take a closer look at this business.

Summary

Pros:

-

Improved performance and market share

-

Asset-backed balance sheet, debt reduced

-

Good cash generation supports 5% yield

Cons:

-

This is a low-margin and highly-competitive sector

-

No specific targets for improved profitability

-

Has disappointed investors before

Profile

About the stock

J Sainsbury is a supermarket chain operating across the UK. It’s classified in the Consumer Defensives sector, within the Food amp; Drug Retailing industry group.

Sainsbury’s floated on the London market in 1973 and is now a member of the FTSE 100, with a market cap of £5.9bn and a recent share price of 248p.

The StockRanks show high scores in all three factors for Sainsbury, combining to give a high StockRank and style rating of Super Stock. This suggests Sainsbury’s could currently offer attractive quality and value metrics, with a positive outlook for earnings:

About the opportunity

Sainsbury’s has been performing well operationally, gaining volume share from rivals and strengthening its balance sheet.

Meanwhile, third and fourth-placed Asda and Morrisons have underperformed somewhat. Both are also under pressure from high debt loads following recent takeovers.

Sainsbury’s shares appear to be reasonably valued, trading close to book value and offering a useful 5% dividend yield. If the company can capitalise on the relative weakness of its key rivals and deliver a sustainable improvement in margins, I think this stock could benefit from a re-rating.

Business amp; Model

What is the company’s history and what does it do?

J Sainsbury was founded by John James and Mary Ann Sainsbury in 1869, with a single store on Drury Lane in London selling milk, eggs and butter.

Rising living standards in the capital at that time meant there was a growing demand for better quality food. Sainsbury’s aimed to meet this need, providing fresh milk from the West Country and “the best butter in London”.

The model proved popular and the business expanded steadily, opening its 100th store in 1903. Sainsbury’s was one of the pioneers of own-branded goods and also logged other sector firsts, including the computerisation of distribution to stores (1961), organic food (1986), and product ranges for allergy sufferers (2002).

Today the group has 600 supermarkets, more than 800 convenience stores, and over 150,000 employees. However, the concept of above-average quality at a fair price remains a core aspect of Sainsbury’s brand positioning today.

Markets amp; Competition

What is the size and state of the company’s market?

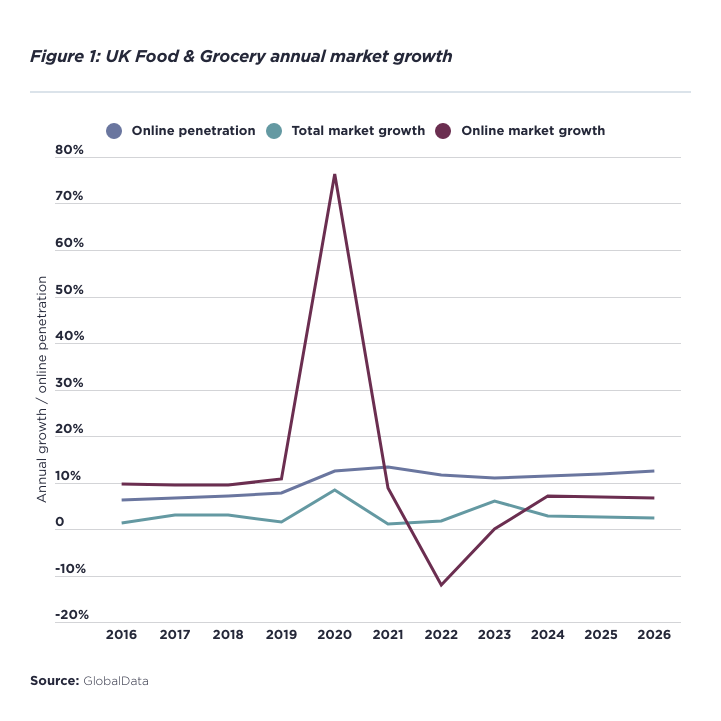

The UK grocery market was valued at about £230bn in 2023. It’s a fairly mature sector; GlobalData analysis suggests the overall size of the market remains unchanged since before the pandemic, albeit with a slightly higher level of online penetration:

Source: Savills / GlobalData

Who are the company’s key competitors?

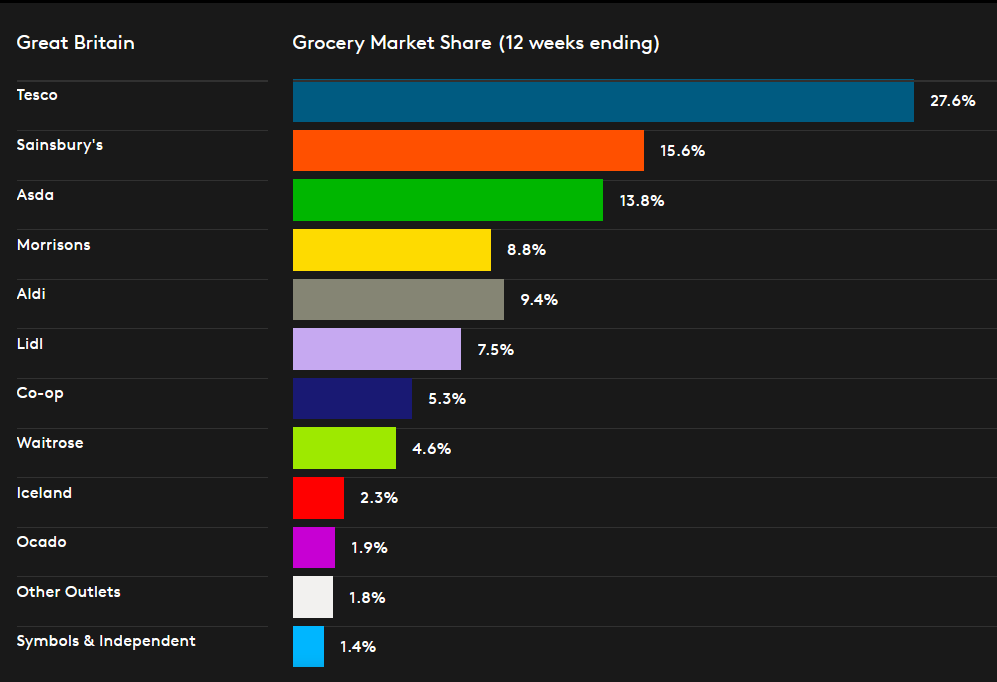

Sainsbury’s is the UK’s second-largest supermarket by market share, behind Tesco (LON:TSCO) but ahead of Asda, Morrisons and the two German discounters:

Source: Kantar Worldpanel UK Grocery Market Share 18/02/24

In general merchandise, Sainsbury’s Argos business also competes with rivals such as Amazon.com (NSQ:AMZN), Currys (LON:CURY) and other retailers.

How does it derive its competitive advantage?

I believe Sainsbury’s brand, positioning and digital operations may give this business some modest competitive advantages.

The company’s heritage and brand positioning have long been associated with quality. Sainsbury’s appears to score better than its main rivals for overall customer satisfaction, according to an industry survey:

Source: Sainsbury Feb ‘24 Strategy Update/CSAT Supermarket Competitor Benchmark

Sainsbury’s Nectar loyalty scheme may also provide some modest competitive advantages. It has 16m members, making it the second-largest such scheme after Tesco’s Clubcard. Nectar members earn points that can be converted to cash savings on grocery spend.

More recently, the supermarket has introduced personalised offers on selected items for online shoppers with Nectar membership.

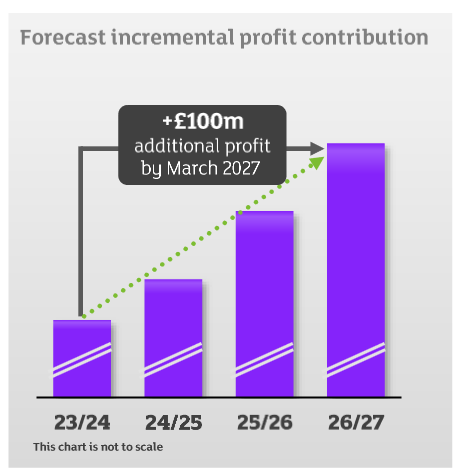

Sainsbury’s is able to use its Nectar data to generate an additional profit stream by selling targeted advertising and promotion services to consumer goods companies. The company expects this to generate £100m of incremental profit by March 2027. That’s potentially material for a company that’s expected to report c.£700m of adjusted pre-tax profit in FY24.

Source: Feb ‘24 Strategy Update

One further source of competitive advantage may arise from Sainsbury’s full range of store formats, which includes directly-operated convenience stores. While Tesco also benefits from this offer, Morrisons and Asda do not, so are unable to capture incremental and higher-margin convenience sales.

Is the competitive advantage durable?

Competitive advantage is hard won and relatively fragile in the UK grocery market. Customers may shop at several different supermarkets and may switch their primary choice if they move house, change jobs, or alternate between online and in-store shopping.

On the other hand, Sainsbury’s has maintained its position as the second or third-largest UK supermarket for many years. I don’t see any obvious reason why this should change.

Financials amp; Ownership

What is the record of growth amp; profitability?

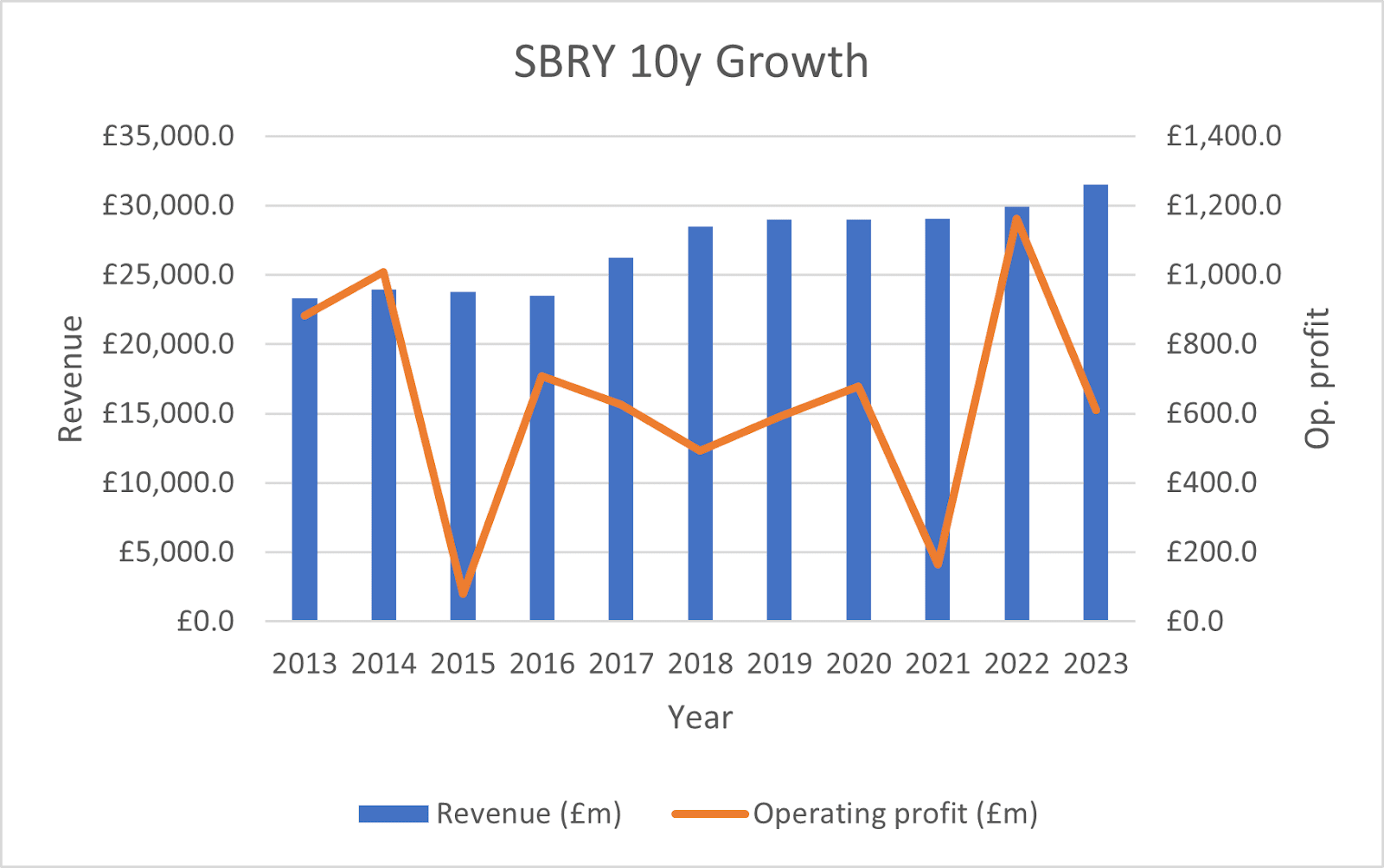

Sainsbury’s revenue has risen at a compound average growth rate of around 3% per year over the last decade, highlighting the maturity and low growth rate of this business.

Without the inflation boost seen over the last two years, I suspect this growth rate would have been even lower.

Reported operating profit has also varied widely over this time, as the company has faced various issues and battled the rapid growth of the discounters:

Like Tesco, Sainsbury was once a more profitable business. But the rapid growth of the discounters from 2013 onwards triggered the start of a price war that’s never really ended. Sainsbury’s margins have never recovered – a problem CEO Simon Roberts is still trying to solve:

Is the balance sheet in good health?

Sainsbury’s balance sheet is in better shape than it was a few years ago. Strong cash generation and some property transactions have reduced non-lease debt to almost zero.

The company’s half-year accounts showed statutory net debt (including lease liabilities) falling £701m to £5,643m. Excluding leases, net debt increased by £375m to £231m due to the upfront costs of a property transaction.

Sainsbury also owns a significant property portfolio. The group’s latest accounts showed land and buildings valued at £7.7bn. These support a balance sheet net asset value of around £3 per share, comfortably above the current share price.

However, realising this value may be difficult unless the business can deliver a sustained improvement in profitability. Sainsbury’s large property estate is a core element of its operating business and cannot be divested.

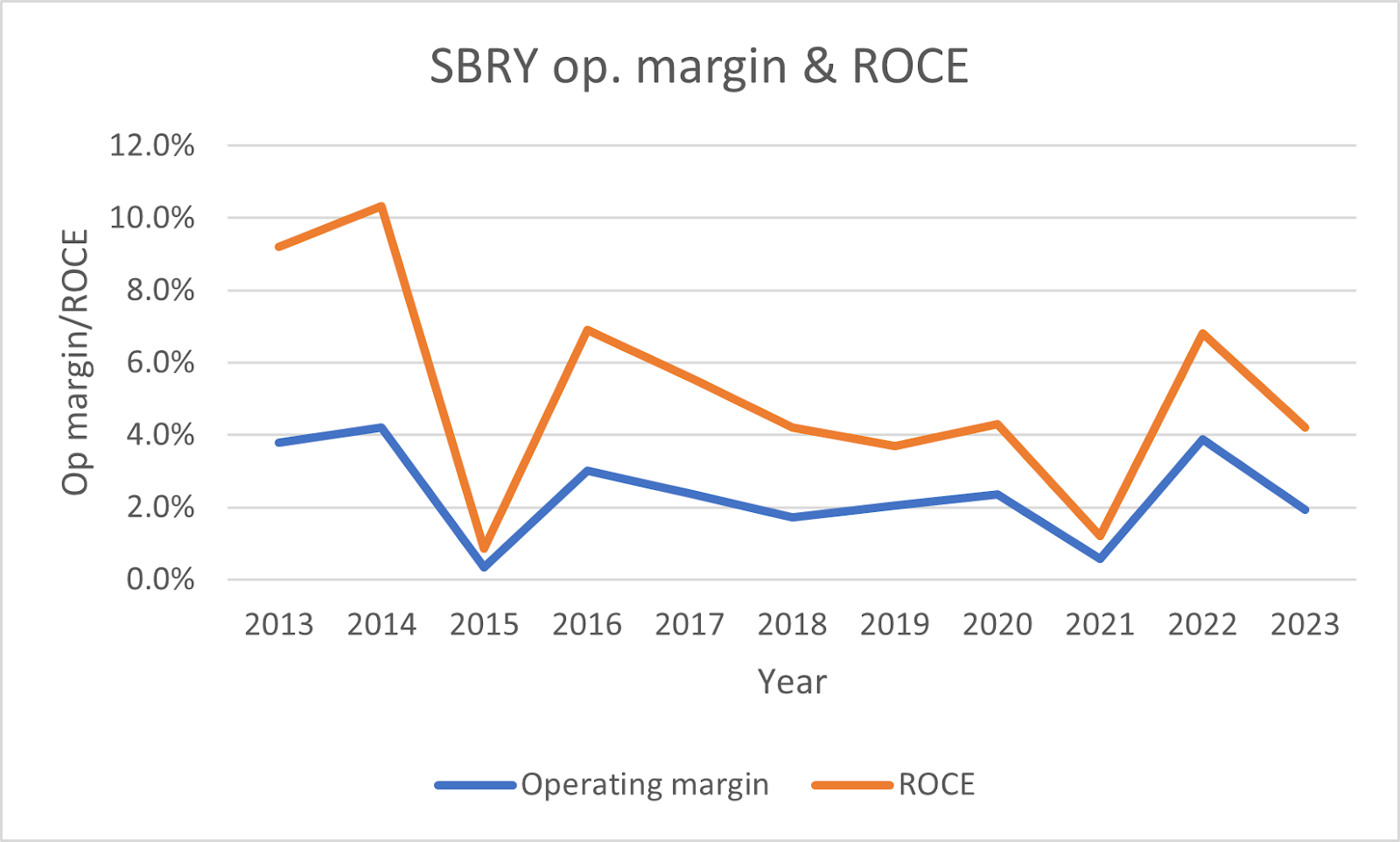

As things stand, I would argue that the group’s low returns on capital employed mean that a discount to book value may be justified.

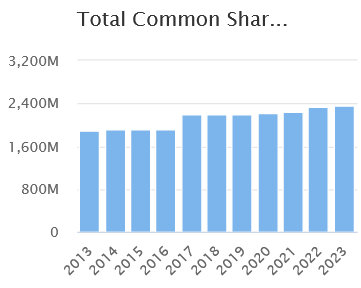

Is there evidence of historic share dilution?

Sainsbury’s has not needed to raise equity directly in recent years. But its share count has still crept higher over the last decade, rising by almost 25% since 2013:

The most significant increase in share count was in 2017, when 261.1m new shares were issued as part of the acquisition of Home Retail Group (Argos).

I believe the main aim of this deal was to increase sales per square foot in Sainsbury’s larger stores. At the time, changing shopping trends meant that the largest-sized supermarkets were starting to look too large. All the big supermarket groups were looking to add additional sources of income to their stores.

However, Argos was an even lower margin business than Sainsbury’s core grocery offering. Although the company stopped reporting general merchandise profits separately in its results a few years ago, I suspect Argos has been persistently margin-dilutive to Sainsbury’s overall business.

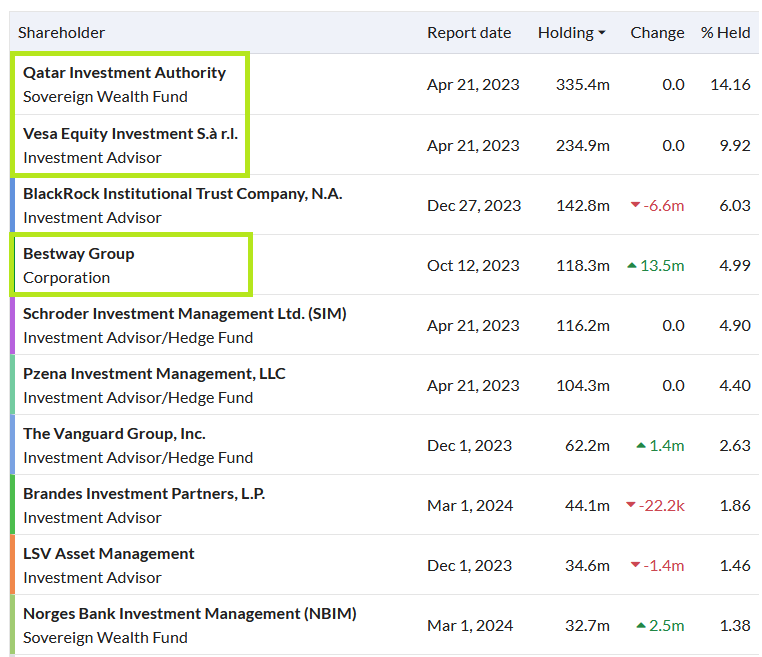

What is the ownership of the company? Does management have stakes?

Sainsbury’s is mostly owned by big institutional investors, but the shareholder register does have a few unusual entries that are worth highlighting:

Sovereign wealth fund Qatar Investment Authority is a longstanding Sainsbury’s shareholder.

Vesa Equity Investment is a Luxembourg-based vehicle controlled by Czech billionaire Daniel Křetínský. Vesa also owns a 27% stake in International Distributions Services (LON:IDS), highlighting its concentrated approach.

Family-owned Bestway Group is the UK’s largest independent wholesaler and also has significant other property and business interests.

Vesa and Bestway’s holdings suggest to me that these specialist investors believe Sainsbury offers significant value and income potential.

Management share ownership: according to Sainsbury’s 2023 annual report, chief executive Simon Roberts is required to hold shares equivalent to three times his salary. The chief financial officer is required to hold twice their salary in shares.

Apart from this, there is no significant boardroom or management shareholding. However, this is not unusual in a FTSE 100 company.

Valuation

How does the relative valuation compare versus industry and sector?

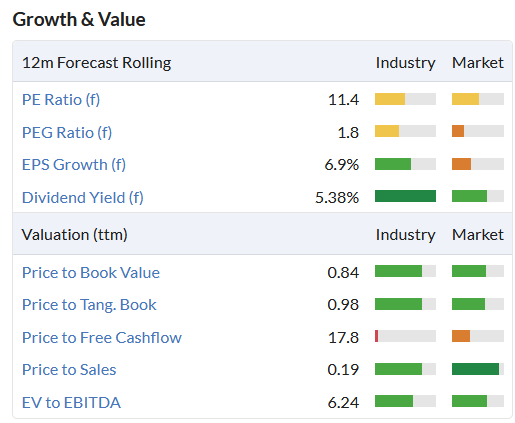

Stockopedia data suggest that Sainsbury’s price-to-earnings ratio is somewhat average, compared to its industry group and the wider market.

However, the stock’s dividend yield and price-to-book value suggest the business may be cheaper than the wider market on these measures:

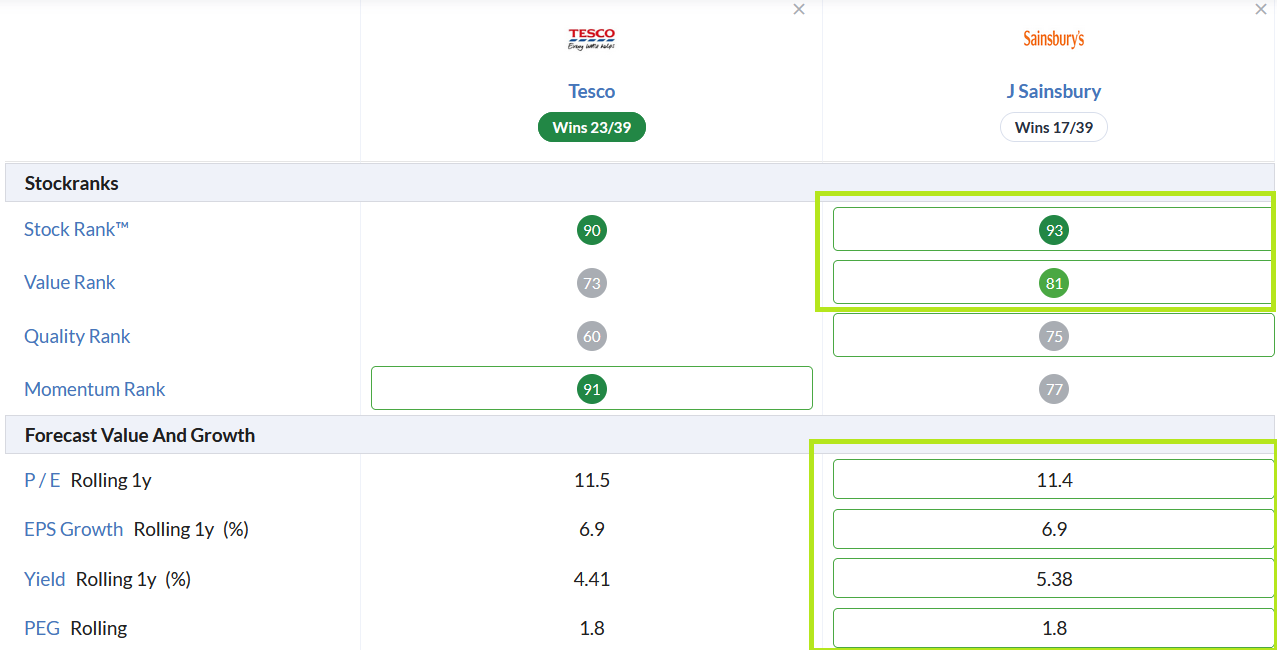

A more focused comparison with key listed rival Tesco suggests Sainsbury is very similarly valued in terms of earnings, only scoring better due to a higher dividend yield:

Sainsbury’s quality metrics are also slightly weaker than those of Tesco, perhaps justifying a more cautious valuation:

What is the stock’s intrinsic valuation?

I have seen discounted cash flow analyses suggesting fair value for Sainsbury’s could be around 350p.

However, given the group’s large capital base and low profitability, I think it makes more sense to value the business in line with its balance sheet net asset value, which I calculate at 305p (H1 FY24).

One point to note is that the group’s balance sheet net asset value is influenced by various assets and liabilities relating to Sainsbury’s Bank. This operation is under review and may be sold or wound down.

Excluding bank-related items, I estimate Sainsbury’s net asset value could be around 325p per share.

Trends amp; Catalysts

Are there any significant macro trends the business is benefiting from?

Macro trends tend to have a similar effect on most supermarkets, as they are all large-scale retailers selling similar products through similar channels.

However, higher interest rates may indirectly benefit Sainsbury, relative to its more highly-indebted peers Morrisons and Asda. These privately-owned businesses are likely to have to devote more of their cash flow to debt servicing than Sainsbury.

In turn, this could mean that Morrisons and Asda will have less opportunity to compete aggressively on price while still investing for the future. Sainsbury CEO Simon Roberts alluded to this in the company’s recent strategy update, when he said:

“Many of our competitors will not be able to make those investments or make them cost effectively.”

Mr Roberts is planning to increase investment in technology and automation to optimise stocking, pricing, and in-store operations. I imagine this could also end up reducing store headcount requirements.

Another example of an area where Sainsbury’s is pushing ahead with investment is EV charging. The company plans to spend £70m installing fast chargers at its stores over the next year or so. At a marginal level, this could help to build customer loyalty, attract floating shoppers and generate incremental revenue from in-store concessions such as cafes.

Are there any catalysts that could drive a rerating in the medium term?

The huge turnover generated by supermarkets means that a small improvement in margins can have a big impact on profits.

For example, based on Sainsbury’s 2022/23 revenue of £31.5bn, a 0.1% improvement in operating margin would add £31.5m to operating profit.

The group’s 2022/23 operating profit was £609m, so a 0.1% increase in margin would have increased operating profit by 5%. I see this as the core element of the investment case.

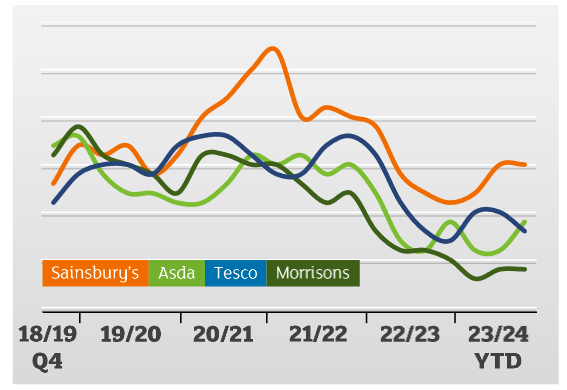

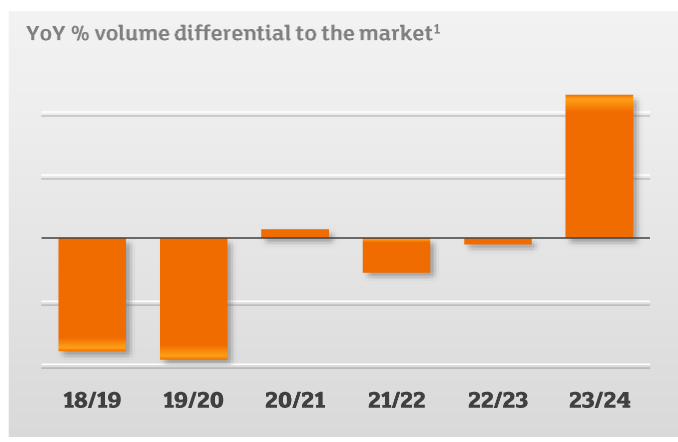

The other opportunity for the business is to continue winning market share. Sainsbury’s says it has been gaining volume share relative to the wider market over the last year:

Source: Sainsbury Feb ‘24 Strategy Update

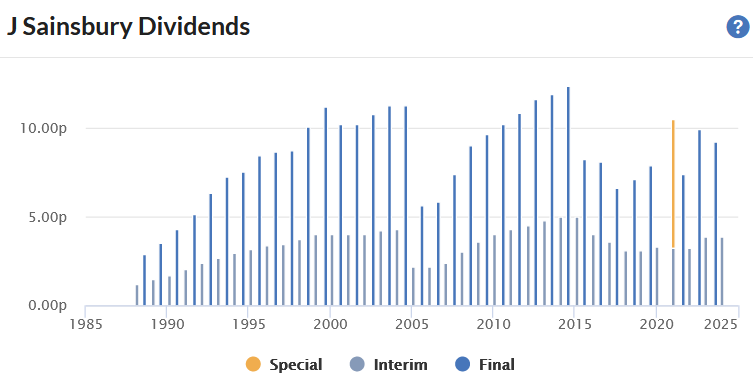

If the company can sustain and extend recent improvements, it could pave the way for a return to a reliable progressive dividend. The company’s dividend history has been mixed, but it is a cash-generative business:

Risks, Threats amp; Hurdles

The UK supermarket sector is likely to remain very competitive. Market leader Tesco has a near-unassailable lead that also provides valuable economies of scale.

However, I think that the biggest risk for investors is that Sainsbury’s will be unable to improve the returns it generates on capital employed.

The company’s share price today is broadly unchanged from 20 years ago:

One reason for this is that earnings have also flatlined, broadly speaking.

In 2009/10 (the oldest annual report on the company’s website), Sainsbury reported underlying earnings of 23.9p per share.

In 2022/23, underlying earnings were 23.0p per share.

This business has not really created any value for shareholders over the last 20 years or so, other than through dividends paid. But the current dividend yield of 5% is no better than the risk-free return available from cash and UK government bonds.

Logically, there’s no point in taking equity risks for a 5% income, unless you believe the investment can generate increased returns in the future.

I think Sainsbury looks in better health and has a stronger outlook than for many years. But this hasn’t yet translated into an improvement in profitability.

I can see some secondary risks, too.

-

The Competition and Markets Authority has already said it will be investigating the use of two-tier pricing in loyalty schemes.

-

Any expansion outside the group’s core grocery business would also be a concern, in my view.

Recent trading amp; news

January ‘24 trading update: Sainsbury’s post-Christmas Q3 statement left full-year guidance unchanged:

“We continue to expect underlying profit before tax in 2023/24 of between £670 million and £700 million, with a strong Grocery performance offsetting weaker General Merchandise and Financial Services contributions. We continue to expect to generate retail free cash flow in 2023/24 of at least £600 million”

Guidance for retail free cash flow of £600m or more gives the stock a free cash flow yield of 10% when compared to the current market cap.

This seems attractive, if sustainable, and suggests the 5% dividend yield will be well supported by cash generation.

Feb ‘24 strategy update: Sainsbury’s has indicated that its annual capital expenditure will rise from £800m to £850m, as the company ramps up investments aimed at delivering improving profit growth and improved returns on capital employed.

Sainsbury’s is also targeting £1bn of cost savings, but did not provide any specific profitability targets in this update.

However, the company did say that it expects to continue generating retail free cash flow of at least £500m per year through to 2027. This should underpin the current valuation and dividend, but does not provide any clear view on growth potential.

Sentiment amp; Outlook

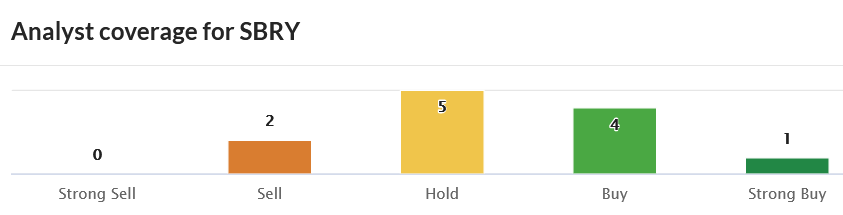

What do the brokers currently think and are they upgrading estimates?

Analysts covering Sainsbury have a consensus rating slightly above hold, although individual views appear mixed.

Earnings estimates have trended modestly higher over the last 12 months and brokers expect a modest improvement in earnings in the 2024/25 financial year:

What would the person selling to us be thinking and who are they?

The stock’s current valuation looks undemanding and Sainsbury’s recent performance has been fairly strong.

However, a seller might argue that the group’s mature, competitive market and structural low profitability means that the opportunity cost of holding the stock is unattractive compared to risk-free or higher-return opportunities elsewhere.

A seller might also be concerned about the slightly vague guidance provided in February’s strategy update.

Conclusions

Sainsbury has not yet proved that it can reverse the decline in profitability seen over the last decade.

However, the stock looks reasonably valued, supported by a decent balance sheet and strong cash generation.

While there are no guarantees, I think the business is in a stronger position now than it has been for a long time. Sainsbury’s improved performance has coincided with more difficult periods for its two closest rivals.

I’d argue that CEO Simon Roberts is right to try and capitalise on this and secure Sainsbury’s grip on the number two slot in the UK market.

On balance, I think the company could deserve its Super Stock rating. But I think there are also many other attractive and credible opportunities in the UK market right now, some of which may be more likely to deliver market-beating returns.

Source: https://www.stockopedia.com/content/does-j-sainsbury-deserve-to-be-a-super-stock-993437/

Anyone can join.

Anyone can contribute.

Anyone can become informed about their world.

"United We Stand" Click Here To Create Your Personal Citizen Journalist Account Today, Be Sure To Invite Your Friends.

Please Help Support BeforeitsNews by trying our Natural Health Products below!

Order by Phone at 888-809-8385 or online at https://mitocopper.com M - F 9am to 5pm EST

Order by Phone at 866-388-7003 or online at https://www.herbanomic.com M - F 9am to 5pm EST

Order by Phone at 866-388-7003 or online at https://www.herbanomics.com M - F 9am to 5pm EST

Humic & Fulvic Trace Minerals Complex - Nature's most important supplement! Vivid Dreams again!

HNEX HydroNano EXtracellular Water - Improve immune system health and reduce inflammation.

Ultimate Clinical Potency Curcumin - Natural pain relief, reduce inflammation and so much more.

MitoCopper - Bioavailable Copper destroys pathogens and gives you more energy. (See Blood Video)

Oxy Powder - Natural Colon Cleanser! Cleans out toxic buildup with oxygen!

Nascent Iodine - Promotes detoxification, mental focus and thyroid health.

Smart Meter Cover - Reduces Smart Meter radiation by 96%! (See Video).

| Online: | |

| Visits: | 1,603,215,016 |

| Stories: | 8,149,335 |

Whistler Blowers, Insiders