Small Cap Value Report (Mon 8 April 2024) - IGP, MIRI, TGP, CBOX, BGO

Good morning from Paul amp; Graham!

I updated my SCVR summary spreadsheet last night, and would you believe that Graham amp; I have already covered 370 unique companies here in 2024 to date! Also with Grahams 2024 share ideas up a stunning 16%, and mine up a not-too-shabby 11%, we’re absolutely thrashing our benchmark of FTSE AIM All Share Index (FTSE:AXX) . Who said it was all doom amp; gloom in UK small caps? Not here it isn’t!

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates amp; results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it’s anybody’s guess what direction market sentiment will take amp; nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps (usually) between £10m and £1bn. We usually avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed – please be civil, rational, and include the company name/ticker, otherwise people won’t necessarily know what company you are referring to.

What does our colour-coding mean? Will it guarantee instant, easy riches? Sadly not! Share prices move up or down for many reasons, and can often detach from the company fundamentals. So we’re not making any predictions about what share prices will do.

Green (thumbs up) – means in our opinion, a company is well-financed (so low risk of dilution/insolvency), is trading well, and has a reasonably good outlook, with the shares reasonably priced. OR it’s such deep value that we see a good chance of a turnaround, and think that the share price might have overshot on the downside.

Amber – means we don’t have a strong view either way, and can see some positives, and some negatives. Often companies like this are good, but expensive.

Red (thumbs down) – means we see significant, or serious problems, so anyone looking at the share needs to be aware of the high risk. Sometimes risky shares can produce high returns, if they survive/recover. So again, we’re not saying the share price will necessarily under-perform, we’re just flagging the high risk.

Links:

Paul amp; Graham’s 2024 share ideas - live price-tracking spreadsheet (2 separate tabs at bottom),

Frozen SCVR summary spreadsheet for calendar 2023.

New SCVR summary spreadsheet from July 2023 onwards.

Paul’s podcasts (weekly summary of SCVRs amp; macro views) – or search on any podcast provider for “Paul Scott small caps” – eg Apple, Spotify.

Other mid-morning movers (with news) -

Tekmar (LON:TGP) – up 14% to 10.0p (£14m) – Contract Wins – Paul – AMBER

Tekmar Group (AIM: TGP), a leading provider of products and solutions for the global offshore energy market, is pleased to announce it has recently secured a number of contract awards, with a cumulative value of approximately £6 million… These contract awards support order intake of approximately £23 million in the financial year to date.

Paul’s view – interesting company, but a very erratic track record. No forecasts available, so I can’t assess it properly. Note overdue receivables, and £18m CLN facility.

Mirriad Advertising (LON:MIRI) – up 29% to 2.25p (£11m) – Partnership with TripleLift – the market seems to like this.

Dismal historical performance with large accumulated multiyear losses. Only achieved £1.8m revenues in 2023. Cash of £6.1m remaining at Dec 2023, so the big question is can it achieve a commercial breakthrough before running out of cash again? The company suggests tantalising potential. I’ll watch from the sidelines I think, as it looks high risk at this stage.

Summaries of main sections

Intercede (LON:IGP) (Paul holds) – 111p (pre-market) £65m – Trading Update – Paul – GREEN

This year end trading update seems to be implying results in line with (increased) expectations – so why not just say so? Superb growth, helped by a large one-off contract win in FY 3/2024. Year end cash has risen greatly, to about a quarter of the market cap, helped by up-front payments by customers. Let’s hope the growth continues.

Cake Box Holdings (LON:CBOX) – up 6% to 171p (£68m) – Full Year Trading Update – Paul – GREEN

FY 3/2024 turned out slightly ahead (c.3%) of expectations. With a generous dividend yield, continued roll-out of stores through franchisees, and a sound balance sheet, I remain positive on this share (despite the historical problems, which now seem resolved).

Bango (LON:BGO) – up 14% to 122.25p (£94m / $119m) – Final Results – Graham – AMBER

These results are below original expectations, as flagged by the company in January’s profit warning. The 2024 outlook is reiterated with the promise of good top-line growth and continued operational progress. Financials now need to catch up with the narrative.

Paul’s Section: Intercede (LON:IGP) (Paul holds)

111p (pre-market) £65m – Trading Update – Paul – GREEN

Intercede, the leading cybersecurity software company specialising in digital identities, today announces the following trading update for the financial year ended 31 March 2024 (“FY24″).

We get a rather strangely worded update today from one of my favourite shares (I hold), that leaves us scratching our heads over whether this is in line with expectations, or above? Confusion is best avoided at this time of day, wherever possible.

There have been a series of positive updates from IGP, as it has demonstrated excellent contract wins over the last c.six months, reflected in a doubling of the share price -

Today it says -

FY 3/2024 revenues c.£20m (Cavendish says this is in line with its latest forecast), and up a highly impressive 66% on the previous year.

On profit it says, rather bizarrely -

The combination of higher revenues and the high operational gearing present in the business is expected to result in improved profitability.

Well yes, I think we’d worked out that profit is going to improve when revenue rises 67%! Why not just tell us profit is going to be in line with expectations? Dodging that makes me wonder if something might have gone wrong?

Cavendish doesn’t seem to have changed its EPS forecast today, which is 7.7p, so it’s probably OK. Remember that contains a one-off large contract win, so we need to use the FY 3/2024 figures with caution.

Cash has come in ahead of Cavendish’s forecast – and this latest figure is about a quarter of the market cap, although some of it will be customers making up-front payments before the services have been delivered –

As at 31 March 2024, gross cash balances totalled £17.2m (2023: £8.3m). The Group has no debt.

Paul’s opinion – I’m hoping that the FY 3/2025 forecasts are set cautiously, as a step back from 7.7p to 3.7p (as currently forecast) would obviously leave little if any scope for the share price to continue rising from its current 111p.

My hope is that IGP could now be establishing a pattern of new contract wins (through resellers), hence rising earnings and a stronger share price. Time will tell if that’s right or not.

I think it’s better if companies stick to a standard format for trading updates, just stating if they’re in line, behind, or ahead of market expectations. Messing about with that format, as we’ve seen today, introduces confusion and probably unnecessary worry.

Cake Box Holdings (LON:CBOX)

Up 6% to 171p (£68m) – Full Year Trading Update – Paul – GREEN

Cake Box Holdings plc, UK’s largest retailer of fresh cream celebration cakes, is pleased to provide a trading update for the 12-month period ended 31 March 2024.

Strong growth across the business resulting in full year profits slightly ahead of market expectations

Revenues up 9% to £38m (remember that it’s a franchising business, so this figure understates the revenues actually generated by the shops)

Shops delivered LFL revenue growth of +4.4%

Raw materials costs have “stabilised”

Efficiency gains.

Overall – profits slightly ahead of expectations.

Stores – 20 new sites opened by franchisees, total stores now 225. Long-term target is 400.

Net cash has improved by £1m in the year, to end at £7.3m.

Broker forecasts – many thanks to Shore Capital for updating us today. It slightly raises forecast profit by c.3%, for 11.3p, giving a PER of 15.1x – that looks a fair price to me.

Note that a particularly good thing about the franchise model, is CBOX can expand its store estate whilst paying out almost all earnings as divis. So shareholders enjoy a dividend yield of c.5.2%. That should grow over time, as the store roll-out continues.

Paul’s opinion – CBOX has had problems in the past, but I think it’s now earned back my trust. On a PER basis it doesn’t look particularly cheap any more, but the generous dividend yield does remain attractive.

Also I should note that the market will now be valuing it on FY 3/2025 forecast of 12.1p, so the PER drops to 14.1x, and it also has a bit of net cash.

For a successful roll-out, with an attractive business model, which could also enjoy improved trading from a consumer recovery this year, I’ve talked myself into staying GREEN.

Shares are only at a similar price to 5-years ago, despite good growth. Although EPS hasn’t increased that much, despite many more stores being opened.

Graham’s Section:Bango (LON:BGO)

Up 14% to 122.25p (£94m / $119m) – Final Results – Graham – AMBER

We already covered the full-year update from Bango in January that missed expectations and saw a 30% fall in the share price.

Today we get confirmation of full-year numbers, showing strong growth as expected despite not hitting original forecasts:

-

Revenue +62% to $46.1m

-

ARR +77% to $8.8m

-

Adj. EBITDA +29% to $6.4m

-

Pre-tax loss c. $9m (last year c. $2m).

The company moves into a net debt position of c. $4m.

As we discussed last time, the most important product from Bango is the “Digital Vending Machine”, a single place where consumers can manage their content subscriptions.

The DVM product is sold to and used by telecoms companies, and had 93 content providers at the end of 2023 – mostly streaming video services such as Netflix and HBO Max.

Outlook: Bango reiterates guidance for 2024.

Q1 revenue up 20% year-on-year.

ARR already reached $11m at the end of March 2024.

CEO comment excerpts:

Our technology is trusted by some of the largest companies in the world who rely on Bango to help them acquire and retain customers….

One major area of focus in 2023 was the ongoing integration of the acquired DOCOMO Digital business, which has materially accelerated our growth. The complexity of the integration was reflected in the low initial purchase price. The integration went well with all $21M of cost synergies realized. With the end of year integration challenges having now been identified and addressed, we have a clear pathway to deliver further operational and cost synergies in 2024…

As consumers add subscriptions in all aspects of their lives, it drives the need for a solution to manage these subscriptions and the opportunity for the Digital Vending Machine to become the standard industry platform for subscription bundling.

More information about the DOCOMO acquisition is available here; the price was only EUR €4m so it is indeed remarkable if $21m of cost synergies have flowed from that deal – it implies an enormous shift in profitability.

Some points to be aware of:

Long sales cycle – selling to telcos on large, multi-year contracts is a lengthy process.

Marketing challenge – Bango helps telcos with their marketing strategy as the Bango bundling proposition ultimately has to be sold to the end-users. A new customer user interface has been developed.

While the sales cycle can be long and a new marketing strategy is required, Bango is still “the simplest and fastest way for telcos to connect to content providers”. For example, Bango provides ready-made commercial terms for telcos to start doing business with all of the content providers immediately.

Financial health?

With the company moving into net debt, I’m curious to see how management feels about this. The Chair’s review of 2023 says:

The Board also determined that it was prudent to carefully manage the pace of investment, given current market conditions. As migrations complete and the free cash flows from the payments business rise, a priority is to use these to build cash reserves, repay any debt and invest in the rapid growth around the DVM.

Bango has one main loan (c. $8m) charging interest at 6%, and it must be repaid over two years, starting in Sep 2024. There is also an undrawn £3m RCF with Barclays.

Graham’s view

I continue to find this one interesting, although it continues to have a lot to prove.

The core product seems to be working very well, and gaining traction with major telcos, and for me that is the main source of excitement. The concept of a single platform where consumers can pick and choose their streaming services makes perfect sense to me. The percentage growth numbers here seem to demand respect.

Where am I less certain?

Firstly, the financials haven’t caught up with the story yet.

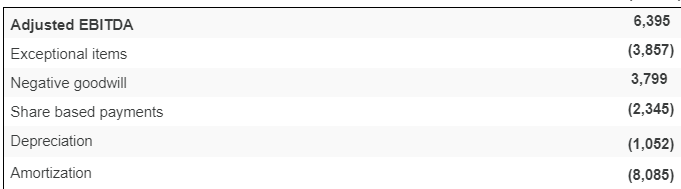

Here is the bridge between adjusted EBITDA ($6.4m) and the operating loss ($5.1m):

Personally, I view the share-based payments as a real cost for shareholders, as the dilution is very real.

Amortisation of $8m is also a real cost. Some people argue that it isn’t, when the only assets being amortised are those acquired during the course of Mamp;A.

However, that argument is much more difficult to make when the company is in the process of adding new intangible assets to its own balance sheet.

Bango’s 2023 cash flow statement shows that $18m of development costs were capitalised, a remarkable figure for a company of this size.

The previous year, nearly $10m of costs were capitalised.

In other words, the company’s reported losses would be significantly higher without this accounting treatment of intangibles.

Overall, then, the financial performance in 2023 is far from good. I’m expecting a huge improvement in 2024, but it’s unfortunate that the 2023 numbers don’t give more to cheer about when it comes to profitability.

(Estimates for 2024 from Singers suggest revenue growth to $53.5m and an adj. PBT of nearly $6m.)

I’m also a little concerned about the company’s headroom.

At year-end, the company did have cash of $4m and an undrawn facility for GBP £3m.

However, its $8m loan will require a $1m principal repayment every quarter, starting later this year.

Given the amount of development spending involved, and possible exposure to swings in working capital (Bango had $22m+ of receivables and $30m+ of payables at year-end), the financial situation does not seem to be as strong as a defensive investor might wish it to be.

We can only trust that with $21m of cost synergies, and with higher payments from telcos likely to hit the company’s coffers over the next 12 months, that the company will be able to avoid any financial stress.

In conclusion: I’m intrigued by the core product at Bango and impressed by the growth achieved so far. However, I’m not ready yet to start giving it the thumbs up.

The StockRanks would be disappointed if I did:

At a market cap equivalent to $119m, it’s currently trading at an ARR multiple of nearly 11x. This would be pricey, even for American investors.

Source: https://www.stockopedia.com/content/small-cap-value-report-mon-8-april-2024-igp-miri-tgp-cbox-bgo-994098/

Anyone can join.

Anyone can contribute.

Anyone can become informed about their world.

"United We Stand" Click Here To Create Your Personal Citizen Journalist Account Today, Be Sure To Invite Your Friends.

Please Help Support BeforeitsNews by trying our Natural Health Products below!

Order by Phone at 888-809-8385 or online at https://mitocopper.com M - F 9am to 5pm EST

Order by Phone at 866-388-7003 or online at https://www.herbanomic.com M - F 9am to 5pm EST

Order by Phone at 866-388-7003 or online at https://www.herbanomics.com M - F 9am to 5pm EST

Humic & Fulvic Trace Minerals Complex - Nature's most important supplement! Vivid Dreams again!

HNEX HydroNano EXtracellular Water - Improve immune system health and reduce inflammation.

Ultimate Clinical Potency Curcumin - Natural pain relief, reduce inflammation and so much more.

MitoCopper - Bioavailable Copper destroys pathogens and gives you more energy. (See Blood Video)

Oxy Powder - Natural Colon Cleanser! Cleans out toxic buildup with oxygen!

Nascent Iodine - Promotes detoxification, mental focus and thyroid health.

Smart Meter Cover - Reduces Smart Meter radiation by 96%! (See Video).

| Online: | |

| Visits: | 1,604,946,703 |

| Stories: | 8,154,730 |

Whistler Blowers, Insiders